🎯Attention, Crypto Connoisseurs and Auto Aficionados! 🚗💰 Ever heard of Cango Inc.? Once a humble car trader, now they’ve got their sights set on 50 EH/s in Bitcoin mining glory by early 2025. With Tencent in their corner and Bitmain’s blessing, could this be the dark horse of the mining sector?

🕵️♂️Deep Dive into Cango’s Cryptoverse

It’s been a minute since we last dissected the underdogs of Bitcoin mining. I’ve been MIA, partly due to a sluggish sector, but mostly because I’ve been nursing a back injury (pro tip: listen to your body, folks!). Today, let’s unravel the tale of Cango Inc. (NYSE: CANG). Why them? Well, while the mining world’s been hit hard, Cango’s had a few lucky breaks, thanks to a share buyback announcement and a non-binding buyout offer. Intrigued yet?

Here’s the kicker: a few moons ago, Cango was just another auto platform with limited growth prospects. Fast forward to today, they’re gunning for 50 EH/s, with 32 EH/s already up and running. How’s that for a plot twist?

So, how’s this daring pivot playing out? Will Cango quietly become a major player in the Bitcoin mining arena? Let’s get down to brass tacks.

🔍Company Overview: From Auto Trader to Crypto Titan

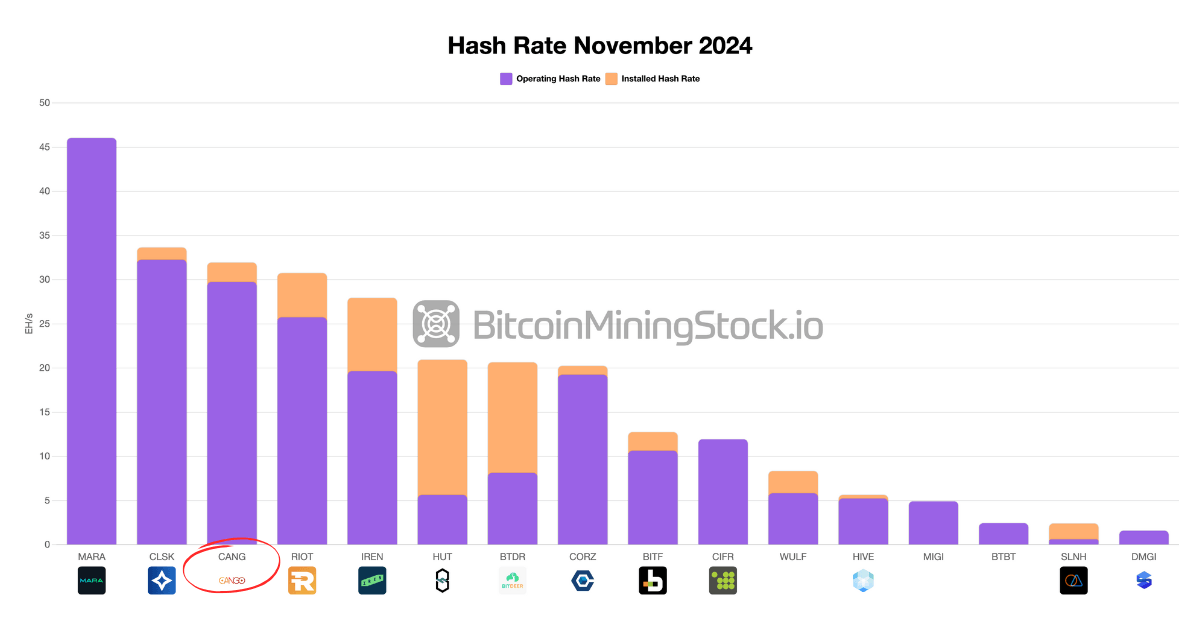

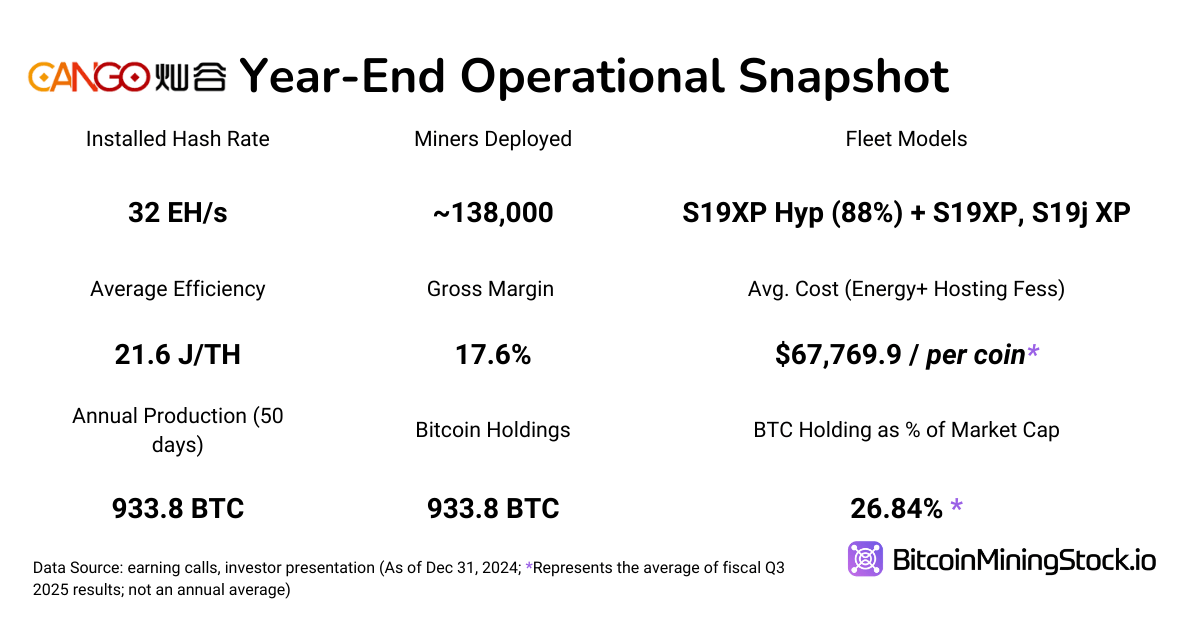

Remember when Cango was just a Shanghai-based auto financier? Those were simpler times. By late 2023, they’d transformed into a key player in China’s automobile trading scene. But then, in a shocking move, Cango announced its foray into Bitcoin mining in November 2024, launching with an impressive 32 EH/s online hash rate. This bold shift has catapulted Cango to the third-largest public Bitcoin miner by deployed capacity.

What’s the secret sauce? Cango acquired operational ASIC fleets straight from Bitmain, with the latter managing operations and maintenance in third-party hosting facilities. Clever, eh? And they’ve managed to avoid China’s crypto crackdown by setting up shop in the US, East Africa, Oman, and Paraguay.

📊Financial Highlights: Revenue Soars, But Profits Lag

💰Revenue & Profitability: The Good, the Bad, and the Ugly

Cango’s pivot to Bitcoin mining has left a significant mark on its financials. Q4 2024 saw revenues skyrocket to RMB 668 million ($91.5 million), a whopping 414% YoY increase, largely driven by Bitcoin mining, which accounted for a staggering 98% of total revenue. However, profitability remains a sore spot. Cango’s gross margin in Q4 was a meager 17.6%, significantly below peers like CleanSpark, which reported a 57% gross margin during the same period.

The culprit? High energy costs and reliance on third-party hosting. Until Cango secures cheaper infrastructure or negotiates better hosting deals, its margin profile will remain under pressure. It’s a classic case of “feast or famine” in the Bitcoin mining world.

💰Balance Sheet & Liquidity: Cash Hoard vs. Liabilities

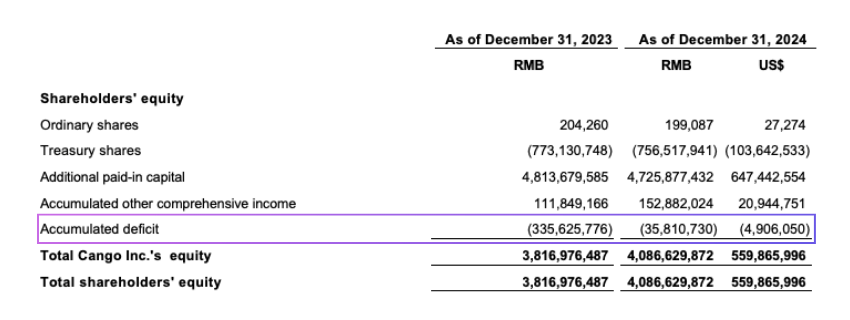

Cango entered 2025 with a robust liquidity position, boasting RMB 2.5 billion ($345 million) in cash and short-term investments. This war chest provides ample runway for growth and cushions against Bitcoin’s notorious volatility. However, total liabilities also ballooned, rising 126% YoY to RMB 1.88 billion ($258 million). This uptick was primarily due to mining acquisition expenses and related operations.

While Cango’s liquidity allows for near-term expansion, improving operational margins is paramount. Without a healthier cash flow, Cango might have to tap external capital, risking equity dilution or increased debt. It’s a delicate dance between growth and solvency.

Comparing Apples to Apples

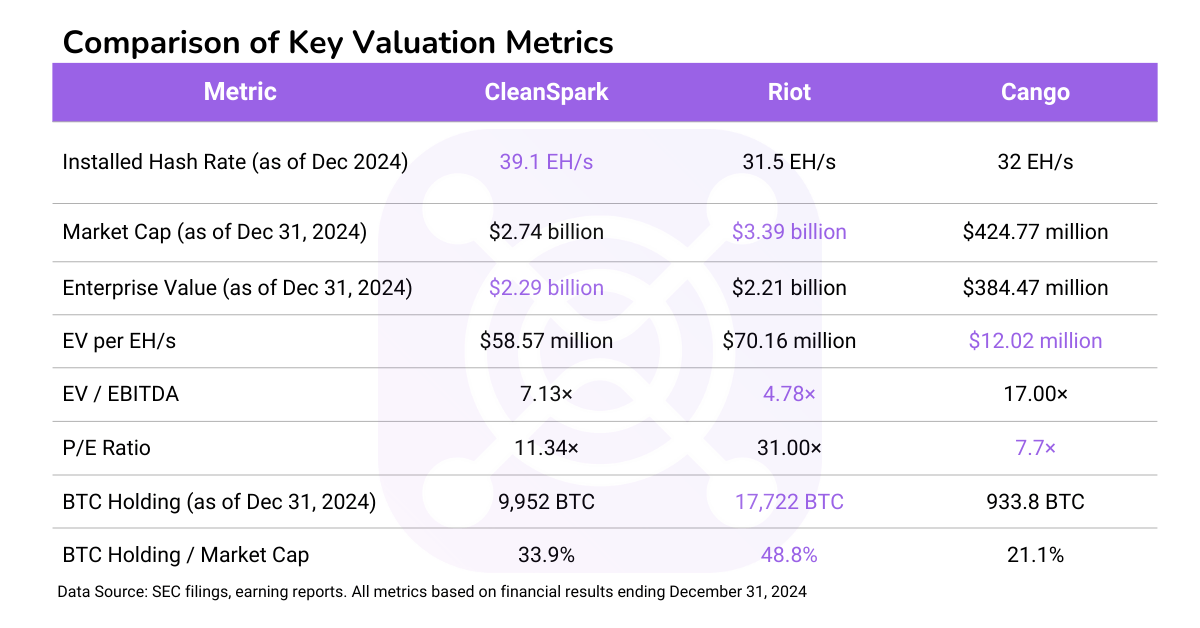

To gauge Cango’s true value, let’s benchmark it against similar-scale Bitcoin miners like CleanSpark and Riot. As of Dec 31, 2024, Cango’s market cap stood at $424.77 million.

- Enterprise Value (EV): $229.2 million

- EV/EBITDA Ratio: 17x

- P/E: 7.7x

- P/S: 2.87x

- Bitcoin Holding / Market Cap: 21.1%

⛏️Mining Operations & Efficiency: The Nitty-Gritty

Cango’s mining journey kicked off with 32 EH/s in December 2024, with plans to scale to 50 EH/s in Q1 2025. Here’s a snapshot of their Bitcoin production in 2025:

- Q4 2024 production rate: 933.8 BTC in just 50 days.

- January-February 2025 update: 1,010.9 BTC mined.

- Projected annual output at 50 EH/s: ~8,500 BTC.

However, this projection assumes linear scaling and ignores network difficulty fluctuations. As global hash rates rise, Cango’s BTC output could dwindle, impacting revenue. The company’s fate hinges on navigating these uncertainties.

Fleet efficiency is another sticking point. Cango’s average J/TH is 21.6, with 90% S19XP Hyd. models and 10% older, less efficient machines. To stay competitive, upgrading to S21 series hardware and transitioning from third-party hosting to self-operated infrastructure could improve margins by cutting hosting fees and energy costs. Failure to do so could spell trouble for Cango’s bottom line.

💰Bitcoin Treasuries: HODL or Fold?

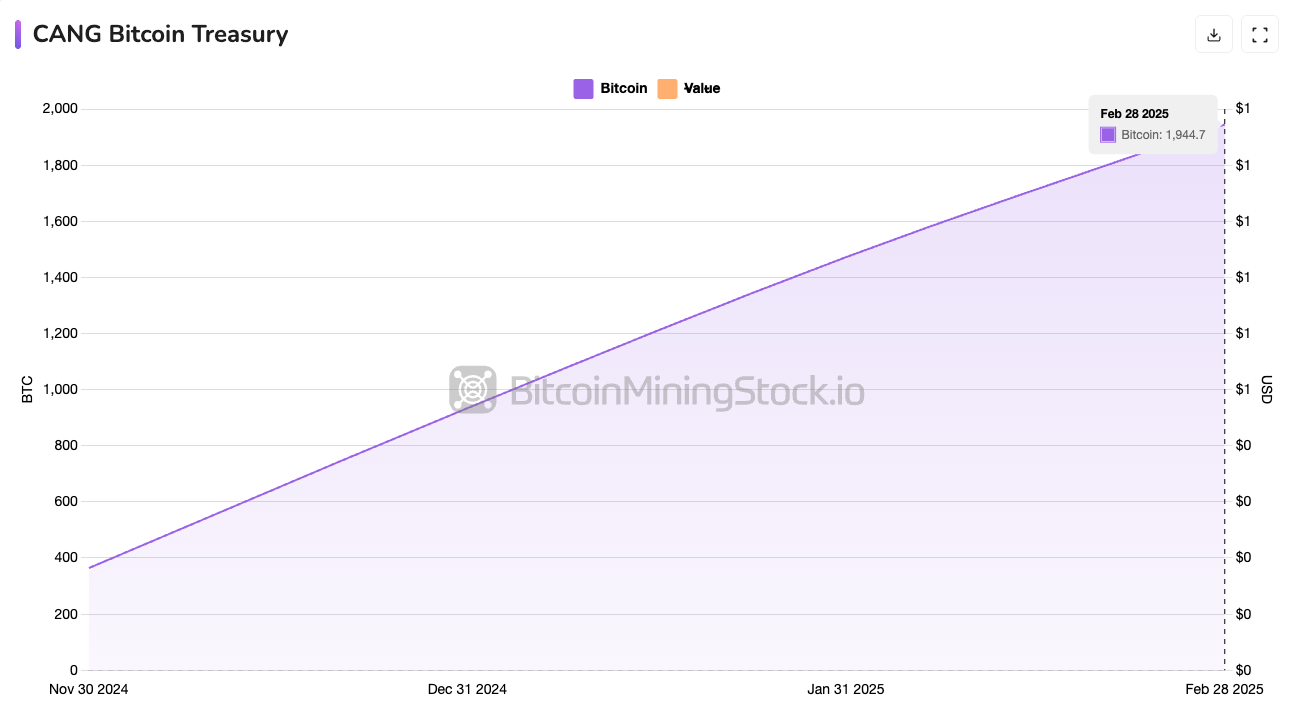

Cango’s adopted a “Mine & Hold” strategy, accumulating Bitcoin rather than liquidating for immediate cash. By February 2025, their treasury ballooned to 1,944.7 BTC. This strategy gained traction when Cango joined the Bitwise Bitcoin Standard Corporations ETF, signaling institutional recognition.

Assuming Cango mines ~8,500 BTC in 2025, their treasury could swell to ~9,500 BTC by year-end. At $100K per BTC, Cango could join the ranks of the largest public BTC holders, potentially reshaping its valuation narrative. However, this strategy introduces liquidity and balance sheet risks. If Bitcoin prices plummet, Cango might have to sell BTC at a loss or seek external funding.

🤔Non-Binding Buyout Offer: Bitmain’s Shadow Play?

In a surprising turn of events, Cango received a non-binding buyout offer from Enduring Wealth Capital Ltd. (EWCL), an investment management company with ties to Bitmain, the world’s largest ASIC manufacturer. This raises intriguing questions:

- Is this an attempt to separate Cango’s Bitcoin mining business from its Chinese roots to mitigate regulatory risks?

- Is Cango turning into a Bitmain-backed mining proxy?

If the deal materializes, Cango could gain direct access to Bitmain’s ASIC supply, reducing hardware costs and boosting competitiveness. However, changes in ownership structure could affect existing shareholders. Investors should monitor the deal’s progress and terms, as it could reshape Cango’s corporate landscape.

💭Final Thoughts: The Road Ahead for Cango

Cango’s transition into Bitcoin mining has redefined its identity. No longer a mere auto platform, Cango now ranks among the largest Bitcoin miners by hash rate. With a stash of BTC on its balance sheet, Cango embodies the “Bitcoin Treasury” trend.

However, the story’s still unfolding. Questions linger around operational efficiency, Bitcoin price stability, and cost structure optimization. Transitioning to self-mining infrastructure could boost long-term margins, akin to MARA’s strategy. The buyout offer from Bitmain-linked entities adds another layer of complexity. If deeper Bitmain integration occurs, Cango could secure discounted ASIC hardware and expedite fleet upgrades.

Challenges remain, though. Cango’s aging fleet, primarily second-hand S19 XP Hyd. models, faces accelerated depreciation. As rivals adopt S21 series machines, Cango risks falling behind in efficiency. Fleet depreciation could further squeeze already slim margins, especially considering the Q4 report didn’t factor in these costs.

It’s worth noting that Cango’s leadership boasts a strong financial background, and Tencent is a top-11 holder. However, Cango’s China-based operations pose regulatory and geopolitical risks, given China’s ongoing mining ban.

Investors in CANG should keep a close eye on:

- Bitcoin production cost relative to peers

- Depreciation and turnover of the older mining fleet

- Liquidity and volatility of BTC holdings under a “HODL” strategy

- Impact of China-based operations on strategic flexibility

- Outcome of the buyout offer and potential Bitmain connections

Will Cango cement its status as a mining heavyweight? Only time will tell. Stay tuned for the next chapter in this thrilling saga!

Read More

- Grimguard Tactics tier list – Ranking the main classes

- Gold Rate Forecast

- 10 Most Anticipated Anime of 2025

- USD CNY PREDICTION

- Box Office: ‘Jurassic World Rebirth’ Stomping to $127M U.S. Bow, North of $250M Million Globally

- Silver Rate Forecast

- “Golden” Moment: How ‘KPop Demon Hunters’ Created the Year’s Catchiest Soundtrack

- Castle Duels tier list – Best Legendary and Epic cards

- Black Myth: Wukong minimum & recommended system requirements for PC

- Mech Vs Aliens codes – Currently active promos (June 2025)

2025-03-30 08:02