As a seasoned analyst with over two decades of experience navigating the complexities of financial regulations and emerging technologies, I find the recent revelations surrounding Coinbase’s legal battle with the FDIC intriguing. The unveiling of these ‘OCP 2.0 letters’ offers a rare glimpse into the often opaque world of regulatory influence on the burgeoning crypto industry.

The FDIC’s initial reluctance to release these documents and subsequent discovery of additional “pause letters” raise serious concerns about transparency and commitment to the legal process, particularly in light of their earlier claims of compliance with court orders. This episode underscores the importance of maintaining a delicate balance between regulatory oversight and fostering industry growth, a challenge that I have witnessed play out in various sectors throughout my career.

The implications of this revelation extend beyond the crypto realm, potentially influencing future policies regarding emerging technologies like blockchain. It is crucial for lawmakers to initiate hearings, as suggested by Paul Grewal, to investigate these practices further and ensure that regulatory bodies act in good faith when interacting with innovative industries.

On a lighter note, I can’t help but chuckle at the irony of an agency tasked with preserving financial stability potentially stifling innovation through overzealous regulation. It seems the FDIC might need a refresher course on “How to Let Go” – a class they could offer in their next regulatory handbook!

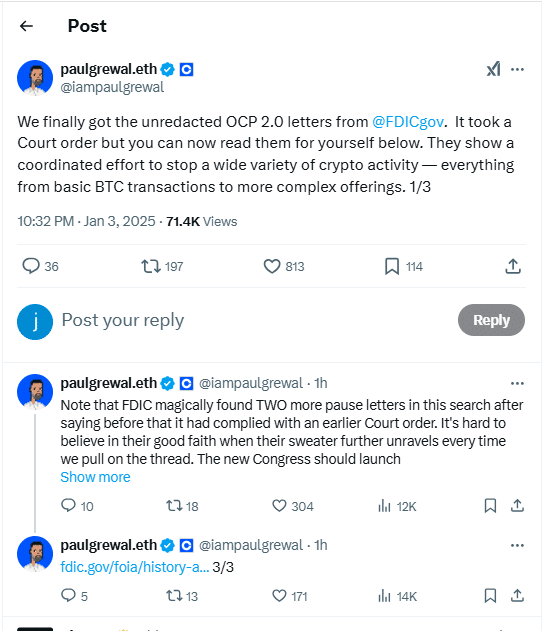

Coinbase’s top legal executive, Paul Grewal, has disclosed that they have obtained unmasked documents from the Federal Deposit Insurance Corporation (FDIC). These papers, called ‘OCP 2.0 letters’, were made public due to a court ruling, providing insights into what Grewal refers to as a joint governmental strategy aimed at limiting various cryptocurrency operations within the United States. The strategy, as described by Grewal, extends across a broad spectrum of cryptocurrency activities.

Based on the records, the FDIC has been encouraging banks to pause or re-evaluate their cryptocurrency services, which range from simple Bitcoin (BTC) transactions to complex financial products tied to digital assets. These communications were part of a larger plan to enable banks to meet compliance requirements and operate in a secure and prudent manner before offering crypto services.

Paul Grewal has openly discussed the potential consequences of these discoveries, advocating for the newly-elected Congress to launch inquiries aimed at delving deeper into these practices.

Initially, the FDIC resisted releasing unredacted letters, which eventually prompted a court order. The judge emphasized that the FDIC had not made a genuine effort in its initial redactions. Contrary to their earlier assertions about following court orders, two more “pause letters” were found later during another search, suggesting questionable transparency and dedication from the agency regarding the legal process.

Background and Legal Battle

The story started in June when Coinbase, using their consulting firm History Associates Inc., filed a lawsuit against the Federal Deposit Insurance Corporation (FDIC). They claimed that the FDIC was organizing ‘Operation Chokepoint 2.0’, a term used by critics to describe what they allege are efforts by federal agencies to restrict the crypto industry’s access to banking services, mirroring a similar initiative from 2013 led by the Department of Justice that targeted various high-risk industries suspected of financial crimes.

As a researcher, I recently discovered that previously redacted letters from the Federal Deposit Insurance Corporation (FDIC) were seeking to disclose the potential influence of the FDIC on banks regarding their engagement with cryptocurrencies. The unredacted versions of these letters now reveal conversations where the FDIC directly advised financial institutions to temporarily halt all activities related to crypto assets, pending additional regulatory clarity or compliance assessments.

This progress could lead to a fresh examination of how organizations such as the FDIC engage with modern technologies, specifically blockchain and digital currencies. Moreover, it adds fuel to the ongoing discussions regarding striking a balance between regulating these sectors and promoting their development.

The Federal Deposit Insurance Corporation (FDIC) hasn’t issued an official comment following the unveiling of the unredacted documents. This revelation might spark more attention from legislators and the general public, which could impact policy-making concerning cryptocurrencies within the American financial sector in the future.

Read More

- Grimguard Tactics tier list – Ranking the main classes

- Gold Rate Forecast

- 10 Most Anticipated Anime of 2025

- USD CNY PREDICTION

- Silver Rate Forecast

- Box Office: ‘Jurassic World Rebirth’ Stomping to $127M U.S. Bow, North of $250M Million Globally

- Mech Vs Aliens codes – Currently active promos (June 2025)

- Castle Duels tier list – Best Legendary and Epic cards

- Former SNL Star Reveals Surprising Comeback After 24 Years

- Maiden Academy tier list

2025-01-03 23:02