Starting from Bitcoin‘s debut in 2009, cryptocurrencies have gained immense popularity. As of 2022, the market was home to over 10,000 distinct tokens, encompassing a diverse range: established coins such as Bitcoin and Ethereum, stablecoins whose values are tied to traditional currencies, novel meme coins, and altcoins backing numerous projects.

Cryptocurrencies offer swift and affordable methods for transferring money, including international transactions. They have limited utility for making payments but can serve as a value depository, though their volatility should be considered. The primary function of cryptocurrencies, however, is speculation – attracting various investors, from individuals to large financial entities, managing vast sums of crypto assets.

Supporters of cryptocurrencies advocate for blockchain initiatives as viable options to bypass conventional financial systems without requiring intermediaries to manage and transfer funds. The absence of regulation in this sphere is viewed as a safeguard for privacy. However, this benefit comes with risks: investors in crypto projects are not shielded from losses or fraud, and the lack of oversight over digital wallets and transfers has made cryptocurrencies an attractive option for illicit activities such as money laundering and criminal transactions.

One reason to regulate: widespread fraud

Markets that follow traditional methods have rules in place for good reason. These include guidelines for public offerings, stringent safety measures to protect the transmission and safekeeping of assets, and regulations against money laundering and terrorist financing to keep ill-gotten funds out of the financial sector.

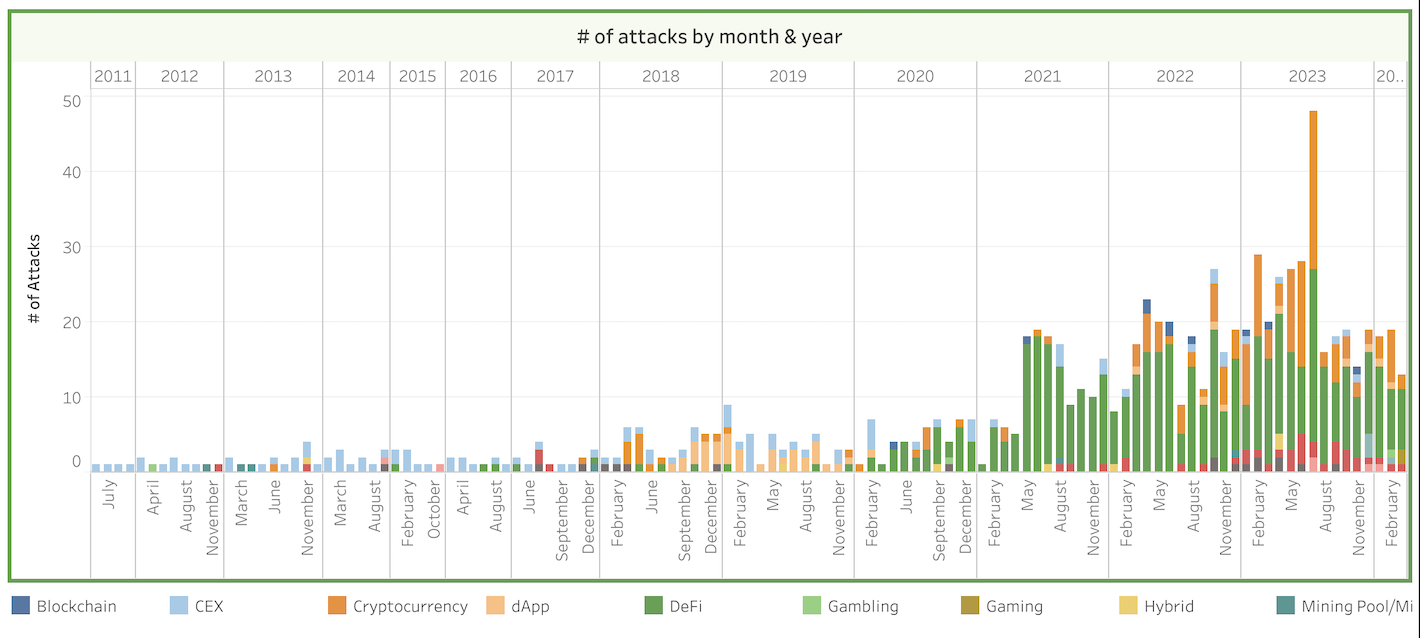

In the realm of cryptocurrencies, fraudulent activities are alarmingly common. According to the “Worldwide Cryptocurrency Heists Tracker,” a platform that records various types of cybercrimes, an estimated $10.5 billion worth of crypto assets were stolen in 879 incidents by 2024. This equates to approximately $50 billion at current prices. The heists encompassed exploits, hacks, flash loan attacks, reentrancy attacks (utilizing vulnerabilities within specific smart contracts), price manipulations, third-party attacks (exploiting the infrastructure of partners), insider attacks, 51% attacks (granting attackers control over networks with a significant token ownership), and governance attacks (manipulating decision-making processes).

Another project, named “Web3,” is thriving with an important mission. This initiative focuses on detecting and preventing various forms of deceitful activities within the crypto world. These include disappearing developers, or “rug-pulls,” which resulted in a staggering $72.5 billion in losses for individuals from cryptocurrency scams. Notable incidents include the Terra/Luna collapse and fraudulent actions by the founders of FTX, Bitconnect, Bitclub, OneCoin, among others. In many cases, these deceitful actors laundered their ill-gotten gains and vanished without leaving a trace.

Anonymity and privacy for money laundering

In the world of crypto, it’s common for people to criticize traditional regulatory systems for not living up to expectations. But here’s the catch: these very same systems may be driving criminals towards unregulated cryptocurrencies instead. Sadly, this shadowy corner of finance has become a preferred method for all sorts of illicit activities. Criminal enterprises have used it for fraud, illegal gambling, drug trafficking, cybercrimes, selling stolen goods, human trafficking, child sexual abuse, murder-for-hire, and more nefarious deeds.

Cryptocurrencies inherently provide anonymity for users, allowing them to manage multiple wallets with only the public addresses being visible on the blockchain. Users can further hide their transaction trails through various methods such as decentralized exchanges, cryptocurrency tumblers, sidechains, chain swaps, privacy coins (which mask both addresses and wallet balances), crypto gambling platforms, and NFTs. Employing a mix of these tools makes it extremely challenging to trace the origin and destination of transactions.

NFT markets have experienced explosive growth, but unfortunately, this surge can be attributed to deceptive practices. Instances of fraud like rug-pulls, scams, insider trading, and wash trading have been rampant in the NFT world. These manipulations make NFTs an attractive tool for money laundering activities. For instance, the record-breaking $532 million sale of CryptoPunk #9998 in 2021 could potentially be a disguised money laundering effort.

In simpler terms, criminals exploit decentralized wallets that ensure anonymity and lenient anti-money laundering (AML) and counter-terrorism financing (CTF) regulations in centralized cryptocurrency exchanges to illegally move funds and finance illicit activities. Notably, Binance, a significant exchange platform, was exposed in a major probe in 2023 for enabling money laundering on its site and processing transactions linked to terrorist organizations like Hamas, Al Qaeda, Palestinian Islamic Jihad, and ISIS. The company and its founder eventually confessed to these criminal offenses.

Are cryptocurrencies broken, and can they be fixed?

Cryptocurrencies serve as practical tools for saving and moving money, carrying both potential risks and rewards for investors. While some criminal activities have exploited their unique traits, the majority of users are legitimate individuals. Carefully crafted regulations won’t harm crypto users but could accelerate its spread beyond tech enthusiasts. The primary reason for regulation lies in the connection between the cryptocurrency market and conventional finance (such as crypto exchanges and fintech applications).

A key element in today’s strategy against money laundering is keeping ill-gotten funds from entering the financial system in the first place. The initial action involves Know Your Customer (KYC), an essential identity verification process that assists in identifying suspect individuals. While not foolproof and susceptible to forged documents or advanced deepfakes, KYC acts as a deterrent for some criminals.

The Financial Action Task Force (FATF) Travel Rule is an essential aspect of cryptocurrency regulations. Under this rule, financial institutions and providers of virtual asset services, including cryptocurrency exchanges, must collect and transmit information about the sender and recipient of transactions in real time to other relevant parties involved. Originally intended for conventional finance, this requirement was expanded to cover virtual assets in 2019.

Analyzing transactions directly on the blockchain is an additional method with value, given that each transaction is recorded in the chain. Yet, due to its intricacy, calling for specialized technical knowledge, this process should not be confused with generating compliance reports.

Compliance is the key to mass adoption of cryptocurrencies

Cryptocurrency supporters argue that regulations go against the fundamental nature of digital currencies, potentially stifling progress. Yet, without widespread use, cryptocurrencies may not reach their full potential. Critics link cryptos to illicit activities and unregulated trading, while banks are hesitant due to regulatory uncertainties.

The European Union led the way in applying anti-money laundering (AML) regulations to crypto assets and is working on a single regulatory framework for all its member states. In contrast, the US has been moving gradually towards crypto regulation. Notably, China has adopted a restrictive stance regarding cryptocurrencies. The true value of cryptocurrencies lies in their integration with traditional finance systems; however, achieving this requires thoughtful and advanced regulatory strategies.

At Dataspike, the role of George Abramishvili is that of a chief revenue officer in this human-focused tech company specializing in AI and regulation. Previously, he acted as a business development consultant for an anti-fraud SaaS platform, where he launched a novel international product aimed at enhancing CPC optimization and safeguarding marketing expenses for prominent brands. With a background of more than five years in both communication and fundraising, George has refined his abilities and successfully obtained approximately $1.7 million in sponsorships and investments for various events and digital projects.

Read More

- Grimguard Tactics tier list – Ranking the main classes

- Silver Rate Forecast

- USD CNY PREDICTION

- Gold Rate Forecast

- Former SNL Star Reveals Surprising Comeback After 24 Years

- 10 Most Anticipated Anime of 2025

- Black Myth: Wukong minimum & recommended system requirements for PC

- Box Office: ‘Jurassic World Rebirth’ Stomping to $127M U.S. Bow, North of $250M Million Globally

- Hero Tale best builds – One for melee, one for ranged characters

- Mech Vs Aliens codes – Currently active promos (June 2025)

2024-04-13 16:27