The text discusses the excitement around real estate tokenization and compares it to publicly traded real estate investment trusts (REITs). It points out that real estate markets do not exhibit the same volatility as stock markets due to the nature of their underlying assets, which are typically not subject to dramatic short-term price swings. The text also highlights the smaller size and lower trade volumes in the tokenized real estate market compared to the cryptocurrency market or even publicly traded REITs.

In the burgeoning crypto sector, real estate tokenization is generally considered a security under the financial regulations of advanced economies like the US, EU, UK, and Australia. In this piece, I delve into the restrictions imposed by securitization in the context of real estate tokenization and argue that the focus should be on digitizing property rights rather than altering land registry systems at their core. Previously, I expounded upon the notion of a “title token” and the development of a cutting-edge blockchain-based estate registry in another article. Here, we critically examine securitization to highlight why progress in the digital economy will be stunted without significant system overhauls.

Securitization explained

As a crypto investor, I’ve always been intrigued by the potential of blockchain technology to revolutionize traditional asset classes like real estate. Historically, real estate has been considered a valuable investment, but its illiquid nature and high upfront costs have made it challenging for smaller investors to participate. However, the tokenization of real estate through blockchain holds great promise.

Although tokenization has gained popularity, it’s important to carefully assess its shortcomings. This examination uncovers the weaknesses of the current model and emphasizes the need for a significant overhaul of the land system in order to bring about genuine advancement.

As a researcher studying the field of digital assets, I can explain that tokenization essentially translates into securitization. This process typically involves setting up a special purpose vehicle (SPV), which could be a corporation or a trust. The tokens issued represent shares or units in this SPV. In some cases, when tokens don’t represent shares or units, they may fall under the broader category of “investment products” or “managed investment schemes,” as defined by various regulations around the world due to the landmark case of SEC vs Howey in 1946.

In economic terms, a security is often seen as a commitment from an individual or entity to undertake a business endeavor in return for monetary investment. Essentially, this involves two parties: one providing the promise and the other supplying the funds. For added context, there exists a secondary market where these securities are exchanged between buyers and sellers.

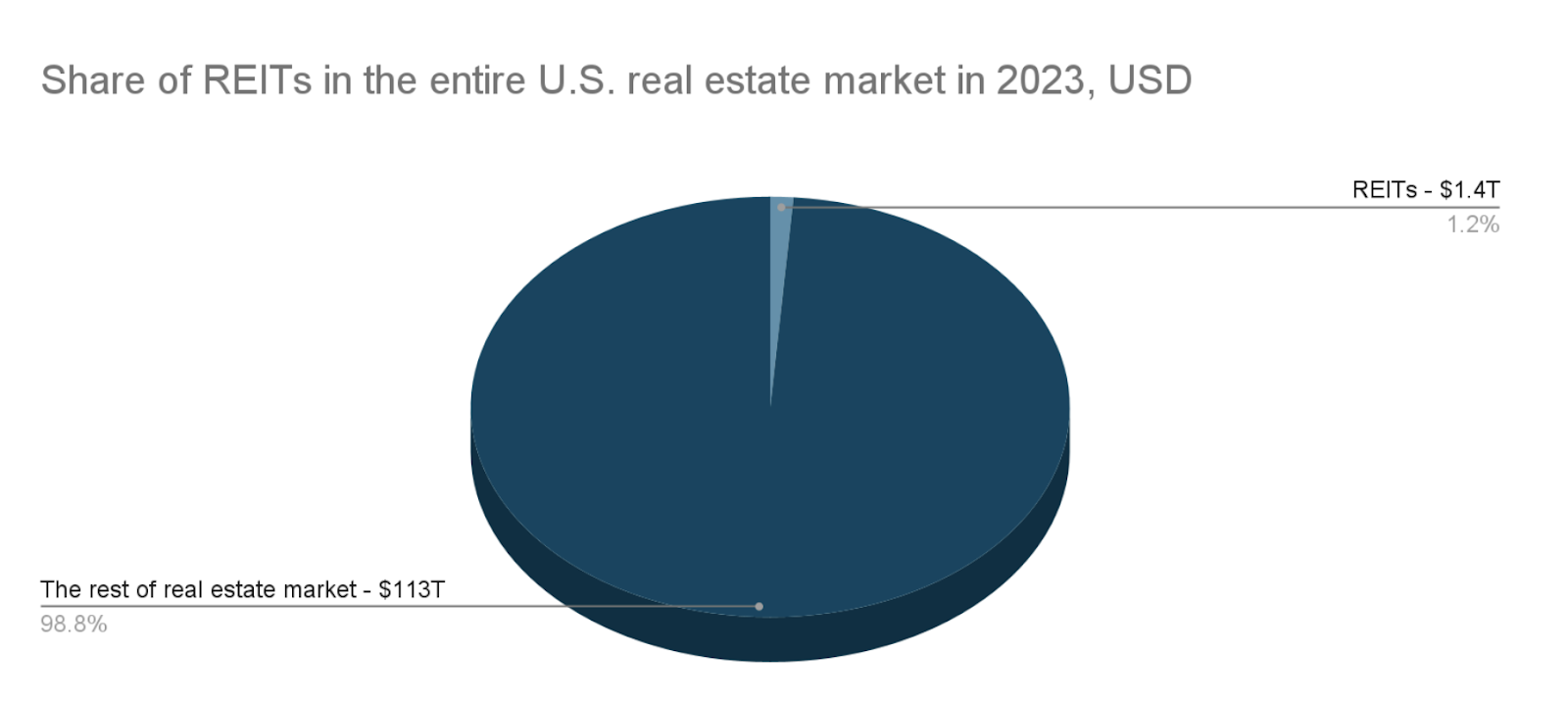

In terms of the broader real estate market in the United States, securitized property holds a minimal share. For instance, the total market value of US publicly listed real estate investment trusts (REITs) was around $1.4 trillion as of 2023, which equates to just 1.3% of the entire estimated US real estate sector, worth approximately $113 trillion.

The gap between securitized real estate and the larger property market underscores the fact that securitization represents a small portion of the overall market. This divide stems from the unique legal characteristics of such arrangements. In essence, securitization refers to an economic interest in someone’s property, which is guaranteed through a legal contract. The party possessing this security does not hold the title to the property itself. Consequently, their rights and abilities to utilize the property economically are restricted.

In simpler terms, a security token signifies the owner’s financial stake in a particular property, while a title token symbolizes the legal proof of ownership of that same property.

Why #tothemoon won’t happen

As a seasoned crypto investor, I’ve witnessed the exhilarating journey of tokenization since its inception during the initial coin offering (ICO) boom between 2016 and 2017. Real estate tokenization has been a particularly captivating area for many, fueled by the overall buzz that pervades our dynamic crypto sphere. The allure of potentially massive returns, derived from market bubbles, is undeniably enticing in this context.

Real estate tokenization is promoted as a method to enhance the market liquidity for property investments. This process is typically described as involving digital technology and fractional ownership, which in turn lower entry barriers and make real estate investment more appealing. Undeniably, this approach carries over the characteristics of the underlying asset.

Real estate prices don’t behave like stock market values, where a company’s growth and innovation can cause shares to soar. Instead, real estate tends to be more stable, with modest fluctuations. It’s rare for the price of one property to spike dramatically while others in the same area remain unchanged. The real estate market generally moves in synchronization, showing similar trends across regions, albeit with slight differences.

REITs and real property tokens

Real estate investment trusts (REITs), which are publicly listed and trade like shares on exchanges, make it sensible to invest in real estate by lowering the entry barriers. These trusts allow individuals to own pieces of companies that own physical property.

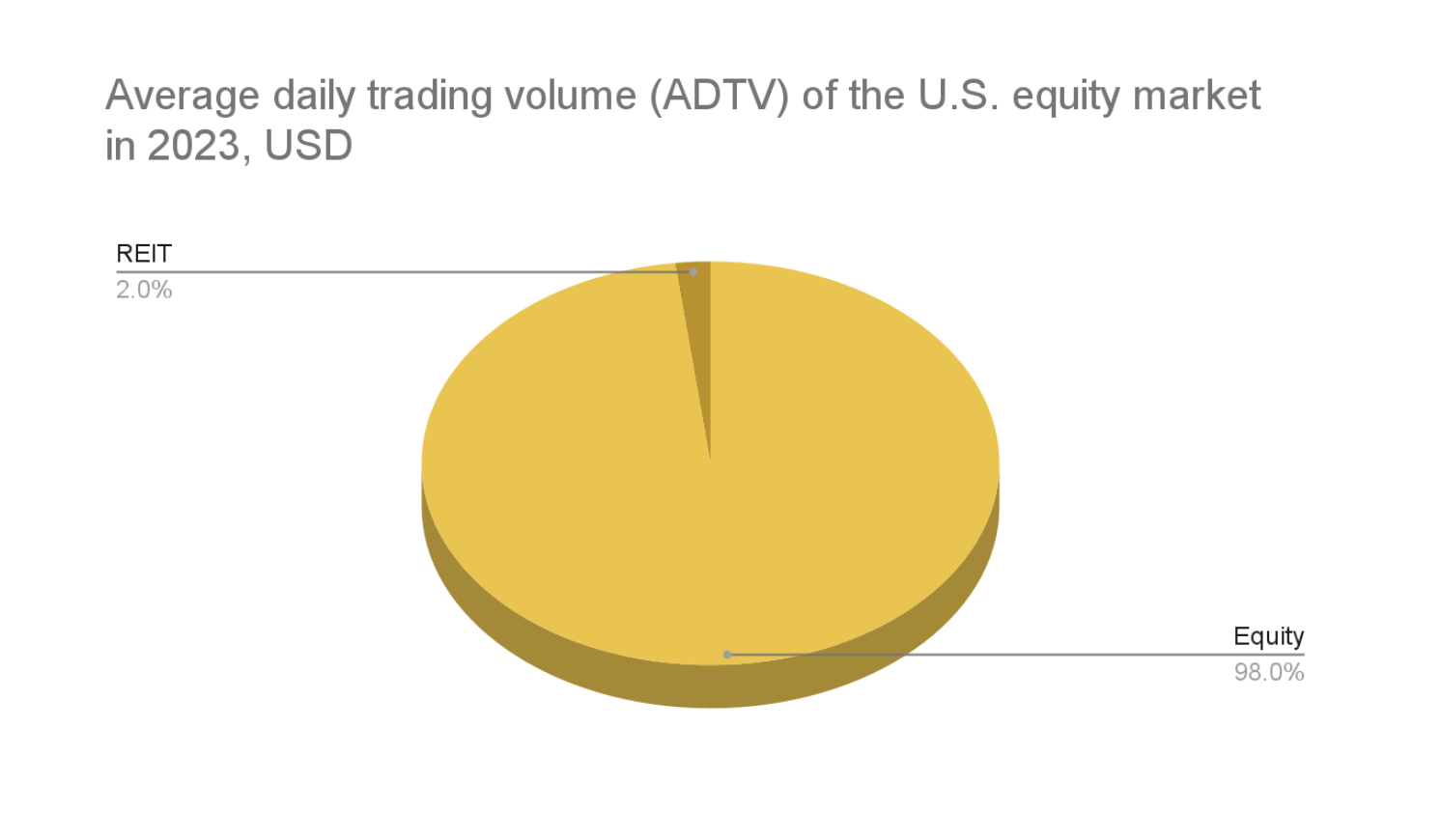

In contrast to significant trading activity in major stock exchanges, which frequently surpassed $500 billion per day in the U.S. equity market during 2023, daily transactions for publicly-traded REITs typically fall within the $10 billion range.

REIT markets exhibit less volatility than the regular stock market. This stability is due to the unique characteristics of their underlying assets – real estate – which generally do not undergo significant short-term price fluctuations. Notably, publicly traded REITs tend to align with broader real estate market trends. The returns of REITs are often in sync with the larger real estate market as they are both influenced by similar economic factors like interest rates, economic expansion, and property values.

The enthusiasm surrounding real estate tokenization appears overly zealous. It’s implausible to assume significant returns from tokenized properties when the broader real estate market is experiencing a slump. However, the digitization of finance brings rational expectations of decreased transaction costs. With Web3 and other digital technologies, security markets become more transparent and accountable, potentially eliminating unnecessary bureaucratic procedures. Consequently, if governments ease regulatory hurdles, REITs can significantly benefit from these innovations.

Now, facts and some concluding thoughts

Let’s delve into some real-life data that reinforces our conversation. One noteworthy platform in the realm of tokenized real-world assets (RWAs) is STM (Stomarket.com). Much like Coinmarketcap.com, it gathers information on various tokens, their total market value, trading volumes, and other crucial market statistics.

As a researcher examining the markets, I’ve discovered a striking contrast between the Real World Assets (RWA) market and the cryptocurrency market. The RWA market, specifically the Real Property segment with its 465 listed tokens on the Securitize Marketplace (STM), boasts a relatively modest capitalization of $226 million and daily trade volume of only $1.7 million. In contrast, the cryptocurrency market, as represented by Coinmarketcap, boasts an astounding capitalization of $2.3 trillion and a daily trade volume of $72.6 billion based on over 8,000 coins and tokens listed (as of May 14, 2024). Deloitte’s analysis paints an even more optimistic picture for the RWA market, estimating its capitalization to be around $16.4 billion in 2022 – still a mere fraction compared to Coinmarketcap’s list, amounting to just 140 times smaller.

To put it simply, securitization isn’t a groundbreaking change, and the hype surrounding the tokenization of real estate markets is premature. While blockchain and related web3 technologies can enhance the efficiency of real estate securitization with the right regulatory frameworks, it’s essential to note that this segment represents only a fraction of the entire real estate market. Therefore, improving efficiencies in this small sector has limited overall impact.

In simpler terms, all ownership records and legal claims to property are kept in traditional government registries, which involve manual transactions and lengthy bureaucratic processes. However, with the emergence of web3 technologies, economic interactions can now transcend borders, occur online, and take place in real-time between individuals without intermediaries such as agents, lawyers, notaries, conveyancers, or registrars. Programmable relationships enable direct transactions, thereby minimizing the need for third parties.

The outdated registry presents a significant obstacle for the progression of the digital economy, as the untapped efficiency is hindered by the antiquated and slow-moving system. The reluctance of the government to modernize and digitize the system impedes its advancement further. In essence, the emergence of securitized and tokenized real property represents a limited attempt to address this inefficiency. However, as demonstrated, it fails to bring about significant change to the overall situation.

Read More

- Grimguard Tactics tier list – Ranking the main classes

- Gold Rate Forecast

- 10 Most Anticipated Anime of 2025

- USD CNY PREDICTION

- Box Office: ‘Jurassic World Rebirth’ Stomping to $127M U.S. Bow, North of $250M Million Globally

- Silver Rate Forecast

- “Golden” Moment: How ‘KPop Demon Hunters’ Created the Year’s Catchiest Soundtrack

- Castle Duels tier list – Best Legendary and Epic cards

- Black Myth: Wukong minimum & recommended system requirements for PC

- Mech Vs Aliens codes – Currently active promos (June 2025)

2024-06-02 17:25